A job-cost report can show a project finished profitable while the bank balance tells a different story. That gap between reported profit and actual cash is where many contractors lose money without noticing.

The cause usually isn’t fraud or carelessness. It’s that the books were set up for a different kind of business. A standard chart of accounts sorts every dollar by category—materials, labor, subcontractors, overhead—without tracking which job generated or consumed it. That works for a retailer. For a general contractor running several jobs at different completion stages, each with retainage withheld and a schedule of values that rarely matches actual progress, it produces numbers that look tidy but tell you little.

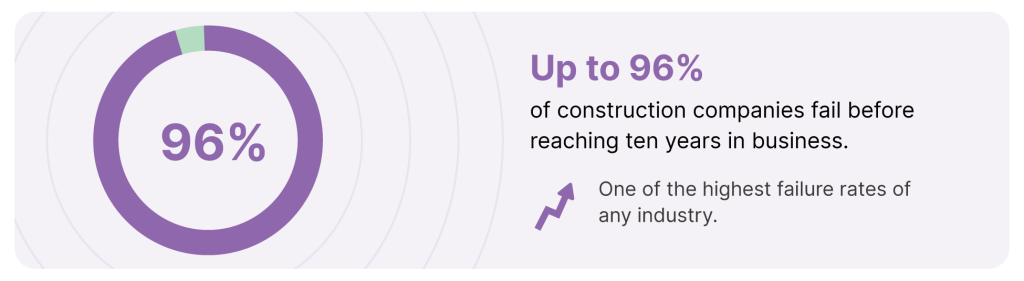

📊 Up to 96% of construction companies fail before reaching ten years in business, and insufficient cash flow is the most-cited cause, according to U.S. Department of Commerce data referenced by Projul. 1 The industry has one of the highest failure rates of any sector — and the books are usually the last place owners look.

Contractors who avoid that fate understand that bookkeeping for construction companies works best as a decision system, not just a tax-prep chore. Here’s what that looks like in practice — and where generic books quietly fail you first.

What Well-Run Contractor Books Actually Do

Effective contractor financial systems are built around projects, not broad expense categories. Strong contractor books typically:

- Track every cost — labor, materials, equipment, subs, overhead — against a specific job

- Produce a monthly WIP report that compares earned revenue to billed revenue

- Record retainage as a separate receivable, not buried in accounts receivable

- Keep certified payroll and multi-job labor allocation clean and audit-ready

- Stay bond-ready and lender-ready without a quarterly cleanup project

The challenge is consistency, not complexity. The mechanics aren’t hard. Doing them every week, on every job, is where most firms fall behind.

Why Category-Based Books Hide Job-Level Losses

Generic bookkeeping fails contractors quietly. It doesn’t throw errors. It just tells you the company made money this quarter without telling you which jobs made it and which ones bled.

The mechanism is simple. When a bookkeeper without construction experience codes a $40,000 lumber delivery to “Materials” and a crew’s hours to “Labor,” the transaction is technically correct and operationally useless. You can’t see that the lumber went to a job you bid too thin, or that labor on the remodel ran 30% over estimate while the infrastructure job carried it. The categories balance. The picture is fiction.

Overhead allocation makes it worse. Costs like insurance, equipment maintenance, and office salaries don’t belong to any single job, but they still have to land somewhere. Most firms spread them using a flat rate based on labor hours — which makes a materials-heavy job look cheaper than it is and a labor-heavy job look more expensive. Bid off those numbers and you underprice the wrong work.

Accurate job costing depends on tracking labor, materials, equipment, and overhead separately because contractors need project-level visibility to make informed pricing and profitability decisions. ²

The fix isn’t more discipline from an overloaded office manager. It’s a chart of accounts and cost-code structure designed for construction bookkeeping built around job costing, where every transaction carries a job and a cost type before it ever hits the ledger.

When you can’t see job-level profit, you can’t protect it.

How Junk Cost Data Quietly Corrupts Your Next Bid

This is the part most contractors miss. Bad job costing doesn’t just distort the job you’re on — it poisons the one you haven’t bid yet.

Your estimate is only as smart as the last ten jobs you coded correctly. When historical costs are miscategorized, your estimating data becomes unreliable, and you start pricing new work off numbers that were never accurate. You win the bid. The bid never had a chance of being profitable. Then you do it again, because the books still say the last one worked.

That feedback loop is how firms with full pipelines run out of cash. More work doesn’t fix bad reporting — it magnifies it. Every additional job multiplies the same blind spots, and growth becomes the thing that exposes them.

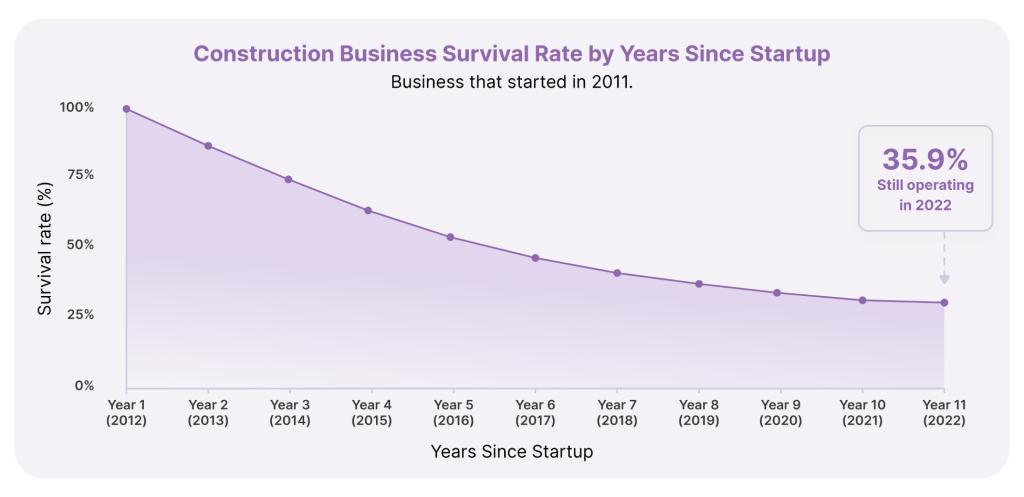

📊 The numbers bear out how unforgiving the cycle is. U.S. Bureau of Labor Statistics data shows only about 35.9% of the construction businesses that started in 2011 were still operating by 2022, as analyzed by TGC CPA — survival rates that decline further as firms age and take on more complex work. 3

Breaking the loop means treating estimating as a live process fed by clean historical data. Material prices move mid-project. Wages shift. Scope expands through change orders that get handled as paperwork instead of the financial events they are. If those changes never make it into job costing, the books diverge from reality and the next bid inherits the error.

Clean cost history is the cheapest estimating tool you own.

When Your WIP Report and Your Bank Balance Disagree

For any contractor running jobs that span more than a single billing cycle, the Work in Progress report is the one document that catches problems before they get expensive. It’s also the one most generic books either skip or get wrong.

A WIP report compares how much revenue you’ve earned on each job — based on percentage of completion — against how much you’ve actually billed. The gap between those two numbers is the whole game. Bill more than you’ve earned, and you’re overbilled. Earn more than you’ve billed, and you’re underbilled.

Why bookkeeping for construction companies depends on accurate job costing

The most common WIP mistake is assuming the budget consumed equals the work finished. Spending 60% of a job’s budget does not mean the job is 60% complete — you might be 40% done and already over. Deltek’s guidance on construction WIP is blunt about the trap: percentage of budget spent and percentage of work completed are different numbers, and treating them as one distorts every report downstream. 4

Why overbilling feels like profit and isn’t

Overbilling inflates your cash position temporarily, which is exactly why it’s dangerous. That money isn’t profit — it’s cash you owe back in future work you haven’t performed yet. Spend it like earnings and the job runs dry before completion.

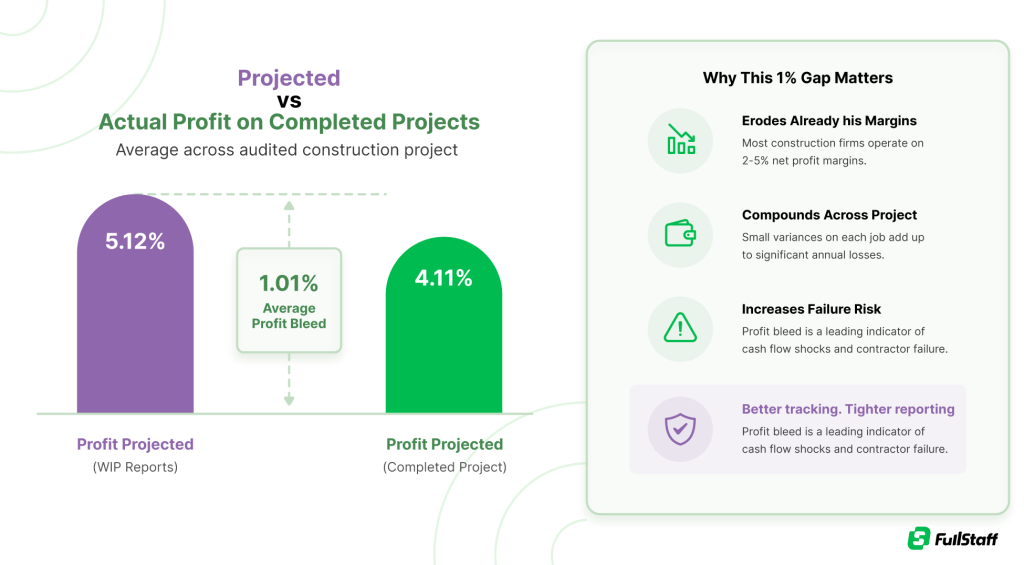

📊 In a multi-year study of audited construction financials, the average difference between profit projected on WIP reports and final completed-project profit ran a little over 1% — a “profit bleed” that the Simplar Foundation identifies as a main cause of sudden contractor failures, since industry margins are thin to begin with. 5

When the WIP report and the bank account tell different stories, believe the report — and find out why before the project closes.

The Cash That Retainage Locks Up Before You See a Problem

Retainage is a structural cash-flow problem disguised as a routine contract term, and generic books make it invisible.

On most contracts, the owner withholds 5% to 10% of every progress payment until the job is substantially complete. The mechanics are well documented: Levelset’s overview of retainage notes that general contractors wait roughly 99 days on average to collect withheld money, 6 while subcontractors — who often finish first — wait around 167 days. That’s months of completed, billed, earned work sitting unpaid.

The accounting problem is that retainage doesn’t behave like normal accounts receivable, but most generic systems file it there anyway. When 8% of every invoice is buried in a single AR line, you lose sight of how much cash is locked up across active jobs — and you make staffing and purchasing decisions as if that money were coming next month.

📊 The portfolio effect is real. Retainage typically reduces working capital 5–10% across active projects and erodes project margin 2–4% through financing and administrative costs, with a $100,000+ impact on a $1 million project portfolio, per Rabbet data summarized by Whittmarsh CPA. 7

The fix is to track retainage receivable as its own line, aged by job, so you always know how much of your earned revenue is held hostage and when each piece is due for release.

Retainage you can’t see is working capital you can’t plan around.

Where Construction Payroll and Compliance Break Generic Systems

Payroll is where construction-illiterate bookkeeping moves from costly to dangerous. The mechanics that retail and service businesses never touch are routine here, and getting them wrong invites penalties, not just inaccuracy.

Multi-job labor allocation is the first break point. A single crew might split a week across three sites, and every hour needs to land on the right job to keep job costing honest. Certified payroll on public works adds prevailing-wage rates, fringe calculations, and weekly reporting that a standard payroll module simply doesn’t produce. Miss a filing and you’re not looking at a messy report — you’re looking at a stalled public contract.

Revenue recognition carries its own compliance weight. Under IRC Section 460, contractors above a gross-receipts threshold — around $29 million, indexed for inflation — must use percentage-of-completion for tax purposes on contracts that span more than one tax year, as Steph’s Books explains in its breakdown of WIP accounting. 8 Smaller firms have more flexibility, but the choice still drives tax timing and bonding capacity, and it shouldn’t be made by accident.

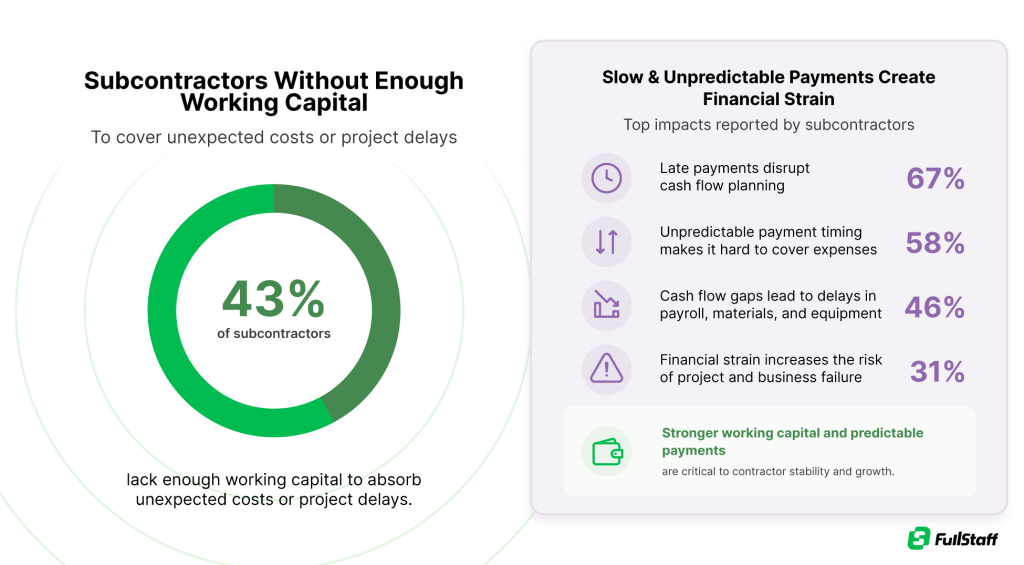

📊 Cash flow pressure continues to challenge contractors across the industry. Recent construction reporting found that 43% of subcontractors lack enough working capital to absorb unexpected costs or project delays, while slow and unpredictable payment cycles continue to create financial strain. 9

This is where many growing contractors find their in-house bookkeeper at capacity — fluent in the day-to-day but stretched thin on certified payroll and compliance. Adding a construction-literate accountant to your team is about bench strength, not replacement.

Compliance errors are the most expensive kind, because you don’t find them until someone else does.

What a Construction-Literate Bookkeeping System Actually Produces

Strong contractor books answer a few questions without drama: which jobs are earning right now, where cash is already committed, and whether your statements are bond-ready and lender-ready when a surety or bank asks.

In practice, bookkeeping for construction companies means more than categorizing transactions. It requires a job-level profit and loss for every active project, a monthly WIP schedule, a retainage receivable aged by job, and certified payroll that holds up to audit. The transactional layer — categorization, invoice processing, reconciliation — increasingly runs on automation, and that’s a good thing. It compresses the repetitive work and speeds the close.

What automation doesn’t do is read a WIP report and tell you a job is quietly underbilled, or flag that your overhead allocation is skewing bids. 10 That’s interpretation, judgment, and oversight — the work of an experienced accountant who has seen the same patterns across dozens of contractors. The right setup uses software to handle volume and people to handle meaning.

The output you’re after is a system that surfaces problems while you can still fix them.

Frequently Asked Questions (FAQs)

Can I use QuickBooks Online for construction job costing?

Yes. QuickBooks Online Plus and Advanced support job costing through class and location tracking, so you can tag costs to specific projects. You’ll need to customize the chart of accounts and set up projects correctly first — out of the box, QBO isn’t configured for construction. For retainage tracking, certified payroll, and multi-phase job costing, most contractors either heavily customize QBO or pair it with a construction-specific add-on. The software can do it; the setup is what determines whether your job costing is actually accurate.

What’s the difference between job costing and regular bookkeeping?

Regular bookkeeping tracks income and expenses by category — materials, labor, overhead. Job costing tracks those same costs by individual project, so you know not just what you spent, but which job you spent it on. That distinction is the entire point of construction accounting. Without job costing, a profitable company can’t tell which projects are earning and which are losing, which makes accurate bidding nearly impossible and hides margin erosion until a job closes.

How much does construction bookkeeping cost?

Most bookkeeping for construction companies run roughly $300 to $800 per month, depending on transaction volume and the number of active jobs. Expect to pay more if you need weekly updates, monthly WIP reports, certified payroll, or retainage tracking across multiple projects. The pricing reflects complexity, not just hours — construction-literate bookkeeping requires job-level setup and reporting that generic bookkeeping doesn’t. Compared to the cost of one underbid job or a stalled public contract, the monthly fee is usually the smaller number.

What is a WIP report and why does it matter?

A Work in Progress (WIP) report compares how much revenue you’ve earned on each active job — based on percentage of completion — against how much you’ve billed. The gap tells you whether each job is overbilled or underbilled. It matters because construction revenue rarely lines up with billing schedules, so without a WIP report your financial statements can show profit that isn’t real. It’s the primary tool for catching cash-flow risk and margin problems before a project finishes.

How is retainage recorded in construction accounting?

Retainage should be recorded as a separate receivable — retainage receivable — rather than buried in standard accounts receivable. It represents the 5% to 10% of each progress payment the owner withholds until substantial completion. Tracking it separately, aged by job, shows exactly how much earned revenue is locked up and when it’s due for release. Filing it inside general AR is one of the most common ways generic books obscure a contractor’s true cash position.

What is certified payroll?

Certified payroll is a weekly reporting requirement on public works projects that documents prevailing wage rates, hours, and fringe benefits for each worker. It’s submitted to the contracting agency to prove compliance with labor laws like the Davis-Bacon Act. Standard payroll software usually doesn’t generate it correctly, and missed or inaccurate filings can stall a public contract or trigger penalties. For contractors doing government work, certified payroll handling is a baseline requirement, not an add-on.

Should a small contractor use percentage-of-completion or completed-contract accounting?

It depends on size and goals. Under IRC Section 460, contractors above a gross-receipts threshold (around $29 million, indexed for inflation) must use percentage-of-completion for long-term contracts. Below that, the completed-contract method is allowed and can defer income recognition. But percentage-of-completion is the professional standard for a reason — it gives you accurate job-level visibility and strengthens bonding capacity. Contractors looking to grow and bid larger work generally benefit from percentage-of-completion despite the added bookkeeping effort.

Can AI replace a construction bookkeeper?

No. AI handles the repetitive transactional layer well — categorization, invoice processing, reconciliation — and using it to compress that work is smart. But it doesn’t interpret a WIP report, catch a skewed overhead allocation that’s corrupting your bids, or manage certified payroll compliance. Those require judgment, oversight, and construction-specific experience. Most growing contractors use automation to speed the routine work and free an experienced accountant for the interpretation and decision support that actually protects margin.

Let FullStaff Handle Your Bookkeeping

Managing construction bookkeeping takes consistency. As projects increase, so do transactions, draws, retainage tracking, change orders, and reporting requirements. Meanwhile, your team is focused on running jobs—not maintaining the books.

Since 2012, FullStaff has helped businesses maintain organized, reliable financial records through dedicated bookkeeping support. Every bookkeeper holds an accounting degree, follows US GAAP standards, and works as an assigned team member—not a rotating resource.

FullStaff can help with:

- Job-cost tracking and project reporting

- Bank and credit card reconciliation

- Transaction categorization and coding

- Accounts payable and receivable tracking

- Monthly close and reporting

- Profit and Loss statements

- Financial reporting and insights

- Catch-up bookkeeping support

- and more

The process is simple: Complete a quick kickoff form so the team can understand your business and workflows, meet with FullStaff to discuss your goals and reporting needs, and get matched with a dedicated accounting professional who helps organize your bookkeeping processes from day one.

👉 Get started with FullStaff today and gain cleaner financials, faster reporting, and better visibility into your business operations. Plans start at $200/month and scale as your business grows.

References:

- 12 Reasons Construction Companies Fail

- Mastering Construction Bookkeeping: A Guide for Success

- The Construction Industry’s High Failure Rate: Avoiding Common Pitfalls

- The Complete Guide to Construction Work In Progress (WIP)

- WIP Accounting – Critical and Often Misunderstood

- The Ultimate Guide to Retainage in the Construction Industry

- 10 Proven Strategies to Accelerate Retainage Collection and Improve Construction Cash Flow

- WIP Accounting for Contractors: How to Track Overbillings and Underbillings

- Cash flow problems continue to plague subcontractors: report

- Construction Work in Progress (“WIP”) Report: Impacts of Over and Underbilling on Bonding